Is it possible to learn invest securities simply by reading? If so name the books

Below is an answer I wrote on Quora to the above question. The question and answer are important to how we all learn our craft of value investing so I’ve decided to post it here as well.

In this post I even show my first ever “analysis” article I wrote less than four years ago to prove how much someone can improve in a relatively short amount of time.

***

Sign up to our mailing list here and get 5 Free Gifts that will help you evaluate stocks better and faster. One of these allowed me to evaluate 3,943 stocks in 40 days manually... And I want you to have it for free.

As Matus said the answer is no.

Books are a great place to learn concepts and theory but if you don’t know how everything works together in the real world it won’t matter. One of the best ways to learn this is by practicing a lot.

How does someone practice value investing?

There are several ways but the best thing to do once you know the basic finance and value investing terms is to begin reading company financial reports – 10K, 8K, Proxy, 10Q’s, etc – then taking notes while reading these financials. Value the company if you know how. And then build an investment thesis from all that information.

It’s then best to show this analysis to someone who knows more about value investing so they can give you feedback on where you can improve. Things and concepts you may have not thought of that you want to add for the future. Etc.

The best way to do this if you don’t know anyone personally who knows about value investing is to start a value investing blog to get feedback. And/or also by posting analysis on sites like Seeking Alpha and Guru Focus.

Beware and don’t take it personally but your first shots at analysis will be crap. Mine was and I post my unedited first ever written “analysis” below to prove this. Be prepared for the suck.

Vodafone Group PLC, ADR, (VOD) info

All information taken from Morningstar – Independent Investment Research, Vodafone’s website, The Motley Fool, or Vodafone’s most recent annual financial report.

Overview:

With 343 million proportional customers (total customers multiplied by its ownership interest), including its 45% stake in Verizon Wireless, Vodafone is the second-largest wireless phone company in the world behind China Mobile. It is also the largest carrier in terms of the number of countries served. Vodafone has majority or joint control in 22 countries and minority or partnership interests in more than 150 total countries. The firm’s objective is to be the communications leader across a connected world. They have four major markets that they break their financials into: Europe, Africa Middle East and Asia Pacific or AMAP, India, and the United States through a partnership with Verizon.

Worried about the next major market crash? Want to protect your investments from that crash? And do you want to learn how to profit from the next market crash by buying undervalued stocks? If so, click here to learn more about our Value Investing Masterclass.

Pros:

1. Huge company operating in more than 150 countries making them more diversified and able to withstand drops in revenues and profits coming from a single region or country.

2. Generates huge free cash flows of at least $8.25 Billion in each of the last 8 financial years. Free cach flow or FCF is basically the money thats left over after expenses, dividends, payments, etc. that the Vodafone can use as it pleases. Generally VOD uses their FCF to increase their dividends, buyback their own stock, acquire other companies, or pay down debt.

3. Current dividend yield of 6.97%, the average company in the S&P 500 has a yield of around 2%. Pays a semiannual dividend in June and November of each year. Also receiving a special dividend from Verizon, $ 1 billion of which will go to paying down Vodafone debt, $3.5 Billion will go to pay a special dividend to Vodafone shareholders in January or February of 2012.

4. FCF/Sales ratio over 16% each year since the 2002 financial year. Anything over 5% means they are generating huge amounts of cash.

5. Interest coverage ratio of 23.4, anything over 1.5 is good. Interest coverage ratio is how many times they can cover the payments of interest on their debt.

6. Payout ratio of around 50% for the dividend meaning the dividend should be safe for the foreseeable future.

7. Raising their dividend an average of 7% per year for the next 3 years.

8. Lower debt/equity than their industy competitors.

9. Growing a lot in Asia, Middle East, India, and parts of Africa. Also still a lot of room to grow in those areas as they are relatively new to them, especially India.

10. Paying down debt with FCF.

11. Gross margin, net margin, and EBT margin all over 17% which is very good.

12. Still a lot of room to grow their revenue through people upgrading to smartphones and paying for data packages which they make more money off of then regular phones.

13. Executive pay is linked to how well the company does, and they encourage their executives and directors to own company stock.

Cons:

1. Still a lot of debt even though they are paying it down, around $40 Billion

2. Most of Western Europe except Germany, are having huge economic problems which has led to lower sales an profits in those areas.

3. The fear or actuality of another global recession would hurt their sales and profits.

4. Problems at Verizon which VOD owns 45% of would hurt future payments from Verizon to VOD.

5. Most of their revenue is generated in Europe where as above, there are big financial problems.

6. Since they are in so many countries they have to deal with many regulations and sometimes even lawsuits from other goverments or companies in those countries.

Final Thoughts:

Overall I feel very good about Vodafone’s prospects to be a great investment for the long term. We are buying them when they are valued at a very good price, especially compared to their competitors. They have huge growth potential in India, a country that has over 1.3 billion people, as they have only penetrated that market by around 10%. They are paying down debt, upping their dividends and receiving a special dividend from Verizon. Even if their share price doesn’t go up over the next few years, which I believe it will by quite a bit, then we are still covered by the near 7% dividend that they are going to keep growing atleast 7% a year for the next 3 years. Also, with their huge FCF they can maybe pay down debt faster, acquire other companies to keep growing, pay more dividends, or buyback their stock.

As always if there are any questions let me know. I believe we will all do well with this stock in our portfolios over the long term.

Jason Rivera

Man that’s painful to look back on. But it’s also inspiring as well.

The analysis is painful to look at because along with the obvious misspellings I didn’t even attempt to correct for whatever reason the analysis doesn’t do anything but spout off random stats I pulled from it financials and places like Morningstar.

That’s not analysis. That’s a regurgitation of facts.

You can see glimpses of analysis in the above piece such as the paying off debt with FCF line. But I don’t take these lines any further. I again chose to just leave off by stating facts. Not what the underlying effects of these things would have on the company. That’s analysis.

At this point I’d been learning about value investing off and on for years but wasn’t improving much because I hadn’t written anything down or shown it to anyone else until the above post.

I actually sent the above “analysis” to a family friend who I was managing some investment money for. Bless their hearts they still stuck with me. They must really love me to have done so 🙂

But the above is also inspiring because in less than four years I’ve gone from the above train wreck to being hired by a prominent investment newsletter due to my analytical ability.

Writing regular 30 to 50 page analysis reports on companies for subscribers and investors I manage money for.

Have written an acclaimed value investment education book teaching everything from the concepts of value investing, to various valuation techniques, how to develop the proper mindsets and processes. Etc.

My stock picks and portfolio have crushed the market in the last four years 2014 And 2015 Portfolio Reviews – Still Kicking Mr. Market’s Ass.

And am told a version of the following on a regular basis – “If I were to go to anyone in the entire company to get a second opinion on my company analysis I would go to your first.”

Posting analysis – and the above one less than four years ago was my very first written remember – jumped my analysis articles, abilities, thought processes, and education into hyper speed.

Doing analysis on a company. Writing it down. Showing it to someone who can give you feedback. Implementing that feedback into future analysis. And then repeating over and over. This is a great way to learn value investing.

But it’s still not the best.

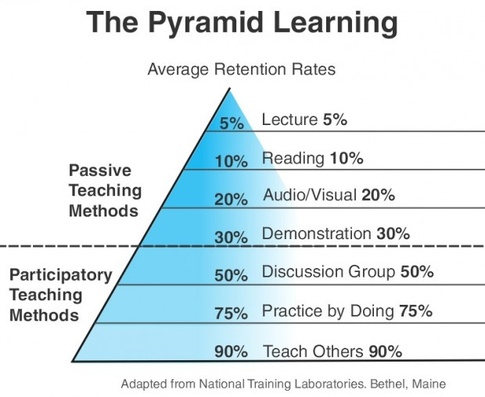

Study after study shows that teaching is the best way to learn any skill and value investing is no different.

This is also another reason you should start a value investing blog so you can teach others.

The below learning pyramid graphic is from the National Training Laboratories showing the best way to learn things.

Now to get back to your original question you see reading at the top showing you only retain ~10% of the information you read and why I struggled before writing things down.

This is how my value investment education jumped into hyper speed by combining practice by doing and teaching.

Anyone asking me how to learn any skill I always tell them to do the same thing that worked best for me.

Doing analysis on a company. Writing it down. Showing it to someone who can give you feedback. Implementing that feedback into future analysis. And then repeating over and over. Then start teaching others as soon as you can to help retain even more information.

If you are looking for book recommendations to learn value investing I recommend going to this post I wrote the other day on Quora What advanced books would you recommend for an aspiring self taught value investor? And this post for more information on How do you learn value investing?

Within the last post is a post on my blog titled 10 Tips To Becoming A World Class Investment Analyst.

I hope this all helps and if you have any further questions please reach out to me at jmriv1986@gmail.com

***

In the comments below please let me know your method and processes for learning and retaining information.