In Jan 2021, I had concluded that STLD was not cheap. There was long-term value but you had to be patient if you wanted a better buying opportunity.

The investment thesis was that:

The main investment risk was that the margin of safety was not enough at the current price then. There was only a 7 % discount to the intrinsic value based on STLD growing at the long-run US GDP nominal growth rate.

But I believed that STLD will report a declining profit in 2021/22 with the opening of the new mill. I do expect the market to have a knee-jerk reaction that will provide you with a better buying opportunity.

In short, STLD was a good company but a poor investment.

For the first quarter ended 2021, the Group had a YTD revenue of USD 3.5 billion and a YTD PAT of USD 435 million. These were better than the revenue and PAT of USD 2.5 billion and USD 191 million for Q1 2020.

There were improvements across the 3 business segments – Steel, Metal Recycling, and Steel Fabrication.

For the Steel segment with accounted for 71 % of the Group’s external sales, growth was driven by price increases.

The Metal Recycling segment which accounted for 13 % of the Group’s external sales benefited from the strong metal demand.

The Metal Fabrication segment benefitted from the robust non-residential construction market. There were increases in tonnage and selling prices.

With all 3 cylinders firing, you should not be surprised by the first-quarter results. But as you can see, the growth is more price-driven than volume-driven. For a cyclical commodity, this is not a sign of sustainable growth.

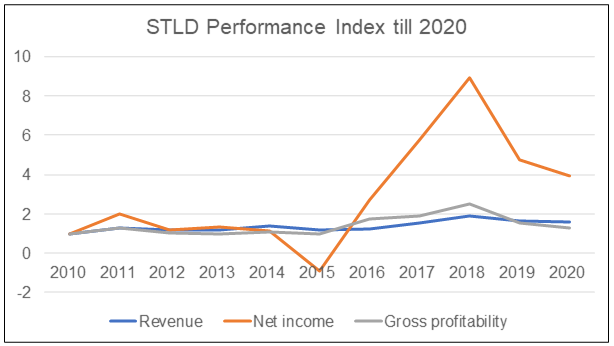

At the same time, from a long-term perspective, I do not see any change to the key metric – gross profitability (Refer to Note 1) as illustrated in the chart below.

If you dig deeper into the performance of the various business segments, you will see that there were no significant changes in 2020. As the chart below shows, you do not see some long-term uptrend.

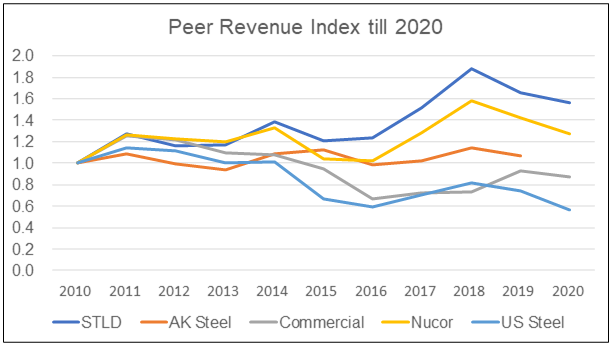

In the context of competitive position, the 2020 performance of STLD relative to its competitors has not changed much. As can be seen from the chart below, all parties suffered a declining business in 2020.

Note: AK Steel was acquired by Cleveland Cliff in 2020 and hence there are no data for 2020

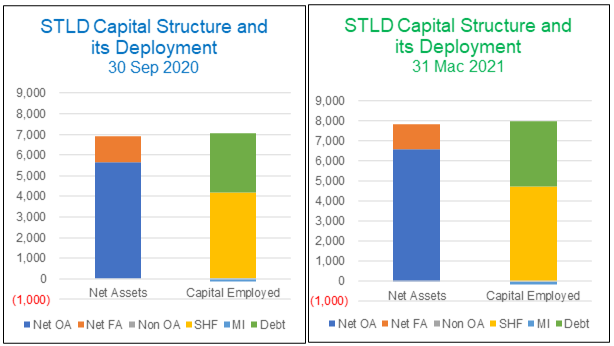

The Group has a total capital employed (TCE) comprising shareholders’ funds, minority interest, and loan of USD 7.83 billion million as of 31 Mac 2020.

In my previous analysis, it was based on the financials that ended in Sep 2020. The chart below showed the changes in the capital structure and its deployment for these 2 periods.

You will note that the Group has more assets now with these funded by both an increase in SHF and Debt. This was to be expected given the new Southwest-Sinton Texas plant under construction.

While there is an increase in the TCE, there is nothing in the 2020 Annual Report to or show a change in the business direction. The fact that STLD will have the same members of the Board and Named Executives in 2021 supports this “status quo”.

Along this line, the new Texas plant will adhere to the same sustainable model as the Group’s other steel-making facilities.

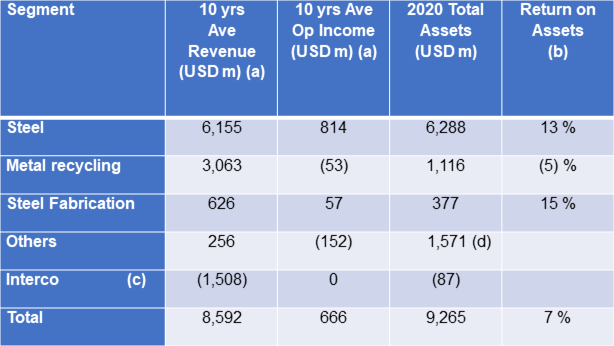

Furthermore, an analysis of the performance of the 3 segments showed similar conclusions as those in Jan 2021. Refer to the chart and table below.

Notes

a) Ave revenue and Operating income based on 2010 to 2020

b) Return on Assets = Ave Operating Income / Total Assets

c) The majority of the Interco sales relate to the Metal recycling segment

d) The majority of the Total Assets under Others is cash

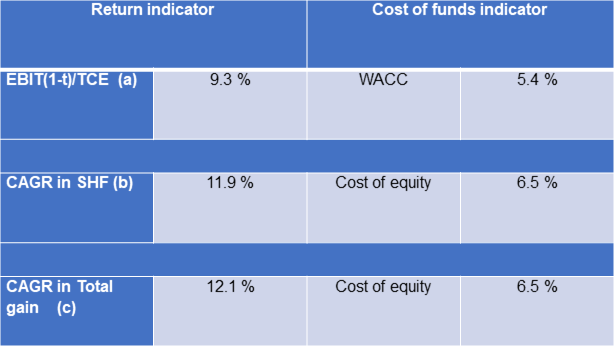

I used the following 3 metrics to answer this question.

As can be seen from the table below, the returns were all greater than the respective cost of funds. In other words, STLD has managed to create shareholders’ value.

Notes

Items | Amount |

Amount spent at the start of 2010 | USD 12.35 |

Total dividends received | USD 6.44 |

Value of shares at end of 2020 | USD 36.87 |

Total gain | USD 30.96 |

CAGR in a total gain | 12.1 % |

The other positive thing is the share repurchase price. I had previously noted that the 2016 to 2019 share repurchases were undertaken at prices that did not seem to add value to shareholders.

Well for 2020, the share buybacks were carried out at much lower prices and closer to book value ie they added value to shareholders.

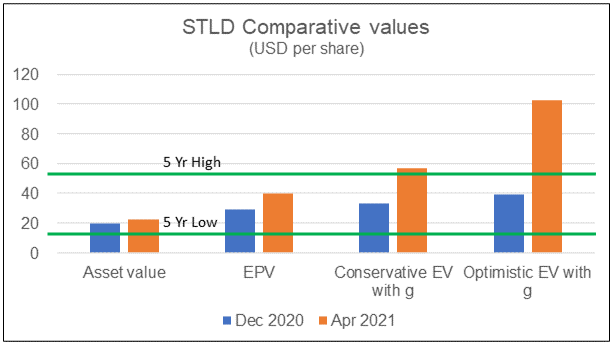

In my previous post, I valued STLD based on the financials from 2010 to 2019. Here I will look at the valuation based on the financials from 2010 to 2020.

The chart and table compared the valuation for the 2 different valuation periods. I looked at several valuation metrics – Asset or Book Value, Earning Power Value and Earning Value with growth.

For the valuation with growth, I considered 2 scenarios:

Note that these were the same growth rates I assumed in my Dec 2020 valuation.

`Table 3: Comparative valuation metrics

`Table 3: Comparative valuation metricsLooking at the chart and table, you could be forgiven to think that there is now a buying opportunity. Don’t jump the gun.

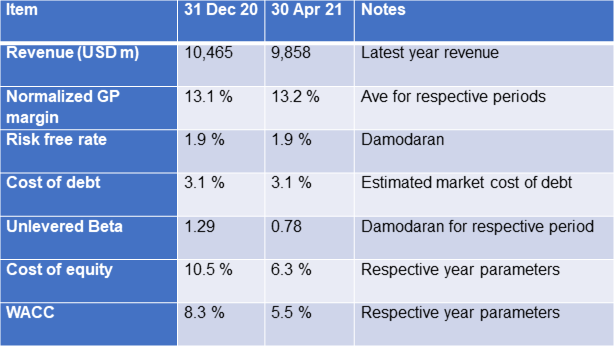

All valuations are based on assumptions and it is worth revisiting these assumptions. For the valuation model, I have used a single-stage Free Cash Flow to the Firm (FCFF) model as per Damodaran.

FCFF = EBIT X (1-tax rate) X (1-Reinvestment rate)

Value = [ FCFF X (1+growth rate) ] / [ WACC – growth rate ]

I derived the EBIT and WACC based on the following:

The key inputs and assumptions used in the valuation are shown below. You can see that the latest WACC is lower than that the last time. This explains why the current values with growth are very much higher than the previous ones.

The analysis showed that the increase in valuation in Apr 2021 is not due to an increase in the “normalized free cash flow” or growth rates. Rather it was due to a reduction in the discount rate.

This is not a characteristic of a growth stock.

Notes

The main culprit for the low WACC for the April 2021 valuation is the Beta. You should not be surprised as 2020 was a Covid-19 pandemic year.

I do not want to get into the debate on how best to derive Betas. However, we should look at the WACC and understand what it stands for. It reflects the time value of money and the risk of the cash flow.

The first question that comes to mind is why is the WACC (aka the risk) lower in a pandemic period? Shouldn’t 2020 be riskier?

There are many studies and discussions about this anomaly. They attribute this to the low interest-rate environment and the economic stimulus. Valuation experts such as Duff and Phelps have suggested adjusting the computed rates to account for these anomalies.

The other question is the valuation model. My model assumes the same WACC for all periods in the future. Does this make sense? We know that 2020 is a Covid-19 year and at best, it will represent the risk for the next few years.

Wouldn’t it be more realistic to then have 2 discount rates?

Rather than turn the whole valuation exercise into a number-crunching one, I would rather take a simple approach. This is to say that a more realistic intrinsic value lies somewhere between the Dec 2020 and the Apr 2021 values.

You may think that this is a wishy-washy answer. Given the many assumptions used, I am not sure whether there is any benefit in adjusting the WACC for 2021 and using two discount rates.

Furthermore, the valuation number is only one piece of the fundamental analysis puzzle. You should devote equal time to getting all the pieces of the puzzle.

There are also strategic insights from comparing the Asset Value with the EPV. This method is attributable to Prof Bruce Greenwald of Columbia Business School. You will note that for STLD, the Asset Values are less than the EVPs.

According to Greenwald, this means that the returns are greater than the cost of funds. Recall that in the earlier section, I have provided the evidence for this. For such a situation to be sustained, STLD must have a strong moat.

However, I have a separate analysis that for STLD, this is Asset Value < EPV is not the true picture. This is because the Asset Value has been “depleted” by its share repurchase programme. If we factor in this share repurchase programme, the difference between the Asset Values and EPV narrows. Refer to “Steel Dynamics: How To Flesh Out The Real Valuation Insights.”

I had concluded in that article that STLD did not have a strong barrier to entry. Its current strong performance could be chipped away and was boosted by financial engineering means. From a long-term investment horizon, I would treat any valuation incorporating growth with a pinch of salt.

For a company to be a growth stock, it must have a growth runway and be in a growth industry. In my Jan 2020 article, I had shown that STLD did not have both these characteristics.

The 2020 and the Q2 2021 performance did not or show a different picture. If there are no secular drivers of growth, the conclusion is that STLD is a growth trap.

But the market price has run away. This is the market looking at the Q1 2021 results. As the analysis has shown, the strong first-quarter performance for the steel operations is the result of price increases. The steel shipment tonnage did not show any growth.

If nothing else, the shipment tonnage validates my thesis. This is not a growth sector and STLD will have to grow by taking market share from its competitors and/or importers.

If you follow this to the logical conclusion it must mean that

In my Jan analysis, I had concluded that STLD was financially sound with a strong management team. It had a business strategy that was aligned with the Group being in a commoditized cyclical sector. In other words, it was a good company. I continue to hold this view taking into account the 2020 results.

But I always differentiate between a good company and a good investment. A good investment is one that enables you to make money. In Jan 2021, I had concluded that there is not enough margin of safety when you value STLD on a long-term basis.

The Jan 2021 investment thesis was the result of my value investing process. I was not trying to judge the next quarter’s market price, but rather to estimate the intrinsic value of the business.

I would be interested to see whether there are other value investors who would have estimated a higher intrinsic value for STLD in Jan 2020. Please let me know as I want to see how our analysis differs.

On the other hand, if you are a trend follower, it is likely that you would have forecast a continuation of the trend as illustrated in the chart below and bought STLD.

However, I do not believe that you should mix investing styles. Each investing style has its own behavioral and mindset requirements. While I have learned both fundamental analysis and technical analysis, I have not been successful in using technical analysis. I keep seeing patterns that were not there.

If you want to be a momentum or trend follower, be an expert in this area and stick to this style. But if you want to be a value investor, stick to value investing and don’t be mesmerized by backward-looking results.

Was I an idiot not to buy STLD? Yes. It is like not buying the winning lottery. Who would not feel so?

But the point about investing is to stick to the process. For the past 15 years of value investing, I knew that my success is a combination of skill and luck. While there were a few occasions that I have lost money, I have a CAGR that was more than the index. This was because following a process minimizes bad luck.

By sticking to my investment process, I

Moral of the story? As a value investor, you will never get the glamour that is associated with the momentum investor or the speculator. I am sure the momentum guys would be gloating over STLD. But hopefully, the value investors make more money in the long run.

We all have different our own approaches in the margin of safety. I look at the margin of safety from 2 perspectives:

As you can see, STLD did not meet these criteria.

From a technical valuation angle, I would ignore the Apr 2021 Earning Value with 4 % growth as this number is very close to the WACC of 5.5 %. This meant that the value using the single-stage model would be “skewed”.

I still believe that when STLD opens the new plant, the Group will experience lower capacity utilization. I still hoped that the market will interpret this negatively and provide a buying opportunity.

Of course, if you are a momentum investor or trend follower, it is likely that you would currently still buy. Unfortunately for you, I am not analyzing STLD on these bases.

Notes

1) Gross profitability is an indicator introduced by Professor Robert Novy-Marx, University of Rochester. It is computed by dividing sales minus the cost of goods sold by total assets…Gross profitability has roughly the same power as book-to-market predicting the cross-section of average returns…Controlling for gross profitability explains most earning-related anomalies and a wide range of seemingly unrelated profitable trading strategies. “The Other Side of Value: The Gross Profitability Premium” – Robert Novy-Marx

2) This defined as TEV/EBITDA. Popularized by Tobias Carlisle, this is a valuation framework that aims to assess the true cost a third party would pay to acquire the company’s cash flow or operating profits. Carlisle analyzed the returns from different valuation multiples and found that the Acquirers’ multiple had the most success identifying undervalued stocks.

“The Acquirer’s Multiple: How the Billionaire Contrarians of Deep Value Beat the Market” – Tobias Carlisle.

3) Unless specifically mentioned otherwise, all charts and tables are produced by the author from readily available SEC filings.

Editor’s Note: The article is from H.C. Eu who blogs at Investing for Value. He is a self-taught value investor and has been investing in Bursa Malaysia and SGX companies for more than 15 years. His value investment experience has been enhanced by both his Board experiences and his contacts with controlling shareholders of many Bursa-listed companies. These have given him a unique opportunity to be able to analyze and value companies differently from other research houses. If you enjoyed this piece, you can find similar pieces and other value investing tips in his blog.

H.C. Eu is not an investment adviser, security analyst, or stockbroker. The contents are meant for educational purposes and should not be taken as any recommendation to purchase or dispose of shares in the featured company. Investments or strategies mentioned may not be suitable for you and you should have your own independent decision regarding them. The opinions expressed here are based on information he considers reliable but he does not warrant its completeness or accuracy and should not be relied on as such. He does not have any equity interests in the company featured.