Rivera Holdings First Acquisition And How You Can Invest

You may have noticed I’ve gone silent in the last month plus. I haven’t posted much on Twitter of Facebook, and haven’t released a new post on the blog since September 29th. This silence is for a great reason though…

Behind the scenes I’ve worked on setting up the legal structure of Rivera Holdings, figured out who can and can’t invest which I’ll talk more about in the coming days, and found two companies to become its first acquisition.

I sent through snail mail and email an activist style letter to a public company stating I was looking to buy them for $20 million, or a 30% premium to its then market value. I’ve still not heard from them at this point. And they will remain a target down the road to acquire because for now I’ve switched gears and found another business to buy that’s even better.

Sign up to our mailing list here and get 5 Free Gifts that will help you evaluate stocks better and faster. One of these allowed me to evaluate 3,943 stocks in 40 days manually... And I want you to have it for free.

The second company I found by accident as I was readying a Letter of Intent to send to the first company above.

Ever since I found them I’ve done a ton of due diligence on the company and its industry, talked in person with the current owner five times so far, The Seller and Rivera Holdings have agreed to a Letter of Intent on an $8 million purchase for the business, and Rivera Holdings is prequalified for the full $8 million amount in a loan to cover the purchase price.

Below I detail the business target more, detail the loan, and tell how you can invest in Rivera Holdings to become part of this deal.

***

Rivera Holdings is now officially and legally open for business.

Rivera Holdings has signed a letter of intent and agreed to an $8 million purchase price with a business owner looking to sell.

Rivera Holdings is prequalified for the full $8 million purchase price through debt financing – minus closing costs and what I have to bring to the table.

And Rivera Holdings is now seeking equity investors to finish closing the deal and begin building wealth for us all.

Below I’ll run these developments down one by one and explain how you can make money.

Rivera Holdings is now set up as a Delaware LLC and is ready for business.

Rivera Holdings has agreed to an $8 million acquisition and both us as buyers and the sellers have agreed to a Letter of Intent on terms. This letter also gives us exclusive rights to work on acquiring the business for 60 days from when it was signed by both parties.

Tired of wasting time learning how to find, evaluate, and value stocks all by yourself? If you're ready to learn more today check out our Value Investing Masterclass by clicking here.

Both I and the Sellers agree the deal can be extended as long as we as buyers are showing movement towards getting the deal done.

The one problem with the Letter of Intent is it keeps me from stating exactly which business it is and which industry the company is in. But below I still tell you some great things about the business Rivera Holdings is acquiring.

If you’re willing to sign the NDA further below the current owner of the business agrees I can then share what the business is, what industry it’s in, and our – Rivera Holdings – specific plans for the business upon closing of acquisition.

For now, let’s get to some things about this great business I can share.

- It’s growing.

It’s on track to produce a little less than $1 million in revenue this year. And since the current owner took over in 2014 it’s increased revenues from $500,000 per year to current level in less than three full years later.

- It’s profitable.

On that almost $1 million in revenue it’s on track to produce an approximate $605,000 in net profit this year. In other words, its net profit margin is on track for an incredible 60% this year.

- There is huge room to cut expenses immediately

After meeting with the owner several times so far and doing my own due diligence I’ve found $115,000 worth of expenses that will get cut immediately without hurting sales or profitability.

This would drop to profitability margins and metrics and increase the net profit margin by 16%. Or an increase from the $605,000 projected for full year 2016 to $720,000. This is counting no further cuts we’re likely to find after taking over operations.

- It’s got valuable property and equipment on its balance sheet.

As I said above the purchase price for the entire business – land, equipment, operations, etc. – is $8 million. The total value of just the land and equipment by recent appraisal and equipment purchases is $8 to $9 million.

In essence, this means we’re buying the land and equipment and getting a valuable 60% + net profit and excess cash producing business for free.

- We’re buying the business at a huge discount to its true value.

As stated above, just the land and equipment is valued between $8 and $9 million. I value current operations between $6 million and $7 million.

This means we’re buying a profitable business, operations, and valuable land and equipment that are worth $15 to $16 million for only $8 million.

- There is massive room for sales/profit expansion at little cost to the business.

A part of current business operations are being expanded and will increase revenues by ~$100,000 to $200,000 per year once completed. Expansion is slated to finish within the next 60 days, or around when I can take over the company depending on closing.

Further expansions to this line of business can and will be done within five years. And prices can raise within the businesses main line of operations 26.7% in this time frame as well. This is talked about more below.

Another part of business operations are being expanded as we speak, will begin generating revenue within next two weeks, and will increase this business sections revenue by 33% to 38%. Or from $96,000 per year to $144,000 to $156,000 per year.

And on top of this, according to the most recent appraisal of the business and property done in August 2016

“The REMOVED has a FAR (Floor Area Ratio) of 25% indicating the area that could be improved/used for more sales opportunities is 38,600 sq feet.”

The above means ~25% of current business property – total property acreage is just under 3.5 acres – isn’t being properly used by the owner.

By utilizing this square footage better it means we could produce an extra $386,000 to $772,000 on $10 to $20 per square foot estimates on commercial lease rates.

Adding all the improvement numbers above together would add another $630,000 to $1,128,00 to revenues. Most of which would drop to profitability – operating and net margins and cash flow – due to low costs to add these new sales opportunities.

Adding and expanding the above business lines would increase sales from ~$930,000 projected for full year 2016 to between $1,560,000 and $2,058,000 million.

Assuming the same net profit margin of 60% and the cost cut mentioned above we would earn $1,051,000 to $1,349,800 in net profit in 2017 and 2018. Or increases in net profit of 42.4% and 55.1% respectively within two years of our take over.

At these levels I would value operations at $10.5 and $13.5 million by themselves. Plus the ~$8 million in property and equipment would take us to $18.5 and $21.5 million for the entire business in one to two years time.

All for an original purchase price of $8 million for the entire business.

- Plus there’s hidden pricing power within the business.

Local and regional businesses selling similar products and services have 26.7% higher prices than current business. And we as new owners will be able to raise prices slowly over several years to reach competitive levels.

One price rise of 8.3% on the company’s major product in the first year will increase monthly revenue by ~$6,000 per month, or $~$72,000 per year. Again, almost all this will drop to profitability.

In the second year, we’d look to raise prices another 4% and in the third year by another 4%. Doing this would further increase revenue on the company’s major product another ~$ 6,000 per month or $72,000 over the two-year period in revenue and profitability.

Using the amounts talked about in the previous section this would increase revenue to $1,632,000 to $2,130,000 million and produce net profits of $1,091,200 to $1,393,000 million in the first year.

In the second year revenues would rise to $1,668,000 to $2,166,000 million and produce net profits of $1,115,800 to $1,414,600.

And in the third year revenues would rise to $1,704,000 to $2,202,000 million and produce net profits of $1,163,200 to $1,465,000 million.

This is with no further cost reductions, further price increases, further marketing – all of which are planned – or adding any other sales opportunities than the ones mentioned above.

At the end of 2019, the end of the above projections, I would value the company’s operations between $11.6 and $14.7 million.

After three years the property and equipment should be worth $10 to $15 million after better utilizing the property and equipment and through land appreciation value.

Adding this value to the value of operations would make the company worth between $21.6 and $29.7 million. In other words, our original $8 million investment will earn us conservative returns between 39.3% and 54.8% each year for three years. Or a cumulative – non-compounded – return after three years of between 117.9% and 164.4%.

At the end of three years we should own a business worth between $21.6 and $29.7 million all for an original $8 million purchase price, with few added costs over the three-year period, little in the way of major new expenses, and still opportunities to grow the company’s operations and profitability further.

And these are ultra conservative estimates because I hate projecting numbers forward like this but have to for business planning purposes.

Barring a major hurricane in the area that would hamper growth, there is no reason the business and land shouldn’t be worth at least $30 million within five years and at least $50 million within 10 years.

All the while producing a ton of excess cash we can use to further enhance this business and buy other businesses. And of course, compound the value of the business and Rivera Holdings private shares for the long-term.

But this isn’t all… The next six things protect our investment even further.

- The revenue model for the business is long-term renewing contracts.

Customers are only allowed to sign yearlong recurring contracts for the company’s main operations. And commercial leasing opportunities are also on long-term – year plus – contracts.

- There’s huge demand for this business in my area.

This business is a 15-minute drive from my house and there’s massive demand for this company’s products in this area. Demand is only growing too as more people move to the Tampa area and more people in the area buy houses.

- The business has a government/regulatory moat protecting us from competition.

There is little competition for this business within a 30-minute drive of where the business is. And due to heavy government/regulatory issues within this companies industry, local and federal governments are likely to never let another type of this business be built or started in this area.

- Even in the event of a major hurricane destroying the entire business current insurance coverage covers everything…

And when I say everything I mean everything; the full value of all property, improvements, equipment, and even revenue protection for a 12 to 24 month period as we rebuild.

- The business requires regular expensive maintenance/upkeep/upgrades.

But all major equipment, maintenance, and necessary expenses and upgrades were completed within the last two years. And most of this equipment has 20 to 40 year expected life cycles.

While the business requires regular upkeep and maintenance, the current owner states there are no major planned expenses or upgrades for the next 10 years. While the two businesses that do compete with us in the area – the only competitors within a 30-minute drive in any direction – both have major multimillion projects planned within the next two years.

- We have a huge margin of safety not only in valuation we are buying at but also in a worst case scenario analysis.

In a worst case scenario analysis assuming a drop in sales of 30% – which is what sales dropped in the last recession – combined with an increase in expenses of 25% – which there’s no precedent for – and the company still produces net income of $197,000 for the full year 2016.

While this huge cut in sales and increase in expenses combine to drop net profits by 65% the company is still profitable in this dire situation.

This worst case scenario analysis also assumes not adding or doing any of the positive things mentioned above: no new ancillary sales opportunities, no upgrading of companies main sales operations, no cost cuts, no price rises, etc.

With this gigantic margin of safety there is almost no way to lose money owning this business over the long-term.

The Short and Medium Term Plan

I’ve already found the $8 million to buy the business – more on this below – so why am I reaching out to you?

- Because I want you involved in building the company by becoming an early equity holder with super voting rights at a heavily discounted rate while we grow and build Rivera Holdings into a billion dollar plus company.

- I’m accomplishing this by raising equity in the parent company of target acquisition Rivera Holdings.

At this point, Rivera Holdings is prequalified for the full $8 million purchase price. The loan will be for $6.8 million and I have to bring $1.5 million to the table including fees, closing costs, and me as the owner having “20% skin in the game on the transaction.”

Having said this I’m selling a 50% equity stake in Rivera Holdings at a $24 million valuation to raise another $12 million as part of this transaction for several reasons.

- To allow you and a few others who have helped me along the way to buy equity in Rivera Holdings at a heavily discounted rate to pay you back for your kindness, wisdom, and friendship. Early investors will also have super voting rights. This means nothing until the company goes public, but early investors in Rivera Holdings private shares will have super voting powers shares upon the company going public. Depending on how this is structured down the road – likely five to ten years down the road – Rivera Holdings private shares will have 2 to 10 times the voting power of Rivera Holdings public shares after IPO. Super-voting shares are always more valuable than regular shares so this is another way early investors in Rivera Holdings will have an advantage over later investors.

- To help you earn safe returns on your investment capital to compound value well into the future. The end goal being building Rivera Holdings into a billion dollar plus company in time.

- Unless a great business falls into our laps at a cheap price I plan to never do another equity sale until we IPO Rivera Holdings. This means you won’t be diluted except in an extremely rare circumstance that’s favorable for us all.

- To ensure a huge margin of safety. As a long-term oriented value investor I hate debt in most cases and I plan to use some of the proceeds of the equity sale to pay off in full, or most of, the $6.8 million loan immediately.

- Under current plans paying off debt in full or partly would leave $3.7 to $6 million left in cash on Rivera Holdings balance sheet compared to $0 to $2.3 million in debt. And Rivera Holdings would own a subsidiary worth $15 to $16 million immediately upon acquisition. Even though it would show up as $8 million in book value on the balance sheet.

- Rivera Holdings balance sheet after acquisition would look something like this: Assets – cash, subsidiary value, etc – worth between $11.7 and $14 million at book value. Again, remember accounting rules don’t care that we value the business a lot higher than the IRS does. With $0 to $2.3 million in liabilities meaning shareholders equity would be between $9.4 and $14 million.

- At this point, I would look to get a $5 to $10 million line of credit at the acquired business – subsidiary – in case of emergencies or necessary upgrades to further increase our margin of safety.

- With the remaining $3.7 to $6 million at Rivera Holdings I plan to send $1 to $2 million to the bank underneath this acquisition to take advantage of business opportunities as they arise, enter into new sales opportunities mentioned above, for advertising and marketing, and for emergencies/repairs of property and equipment as they arise. With current level of expenditures this money should last more than five years. And this doesn’t include any profits or cash produced by the acquisition in those five years.

- The remaining $2 to $4 million will be left at Rivera Holdings and I’m going to invest this money in safe, undervalued, profitable public company stocks as I’ve done over the past five years producing returns of 31.1% on average – not compounded – each year over the last five. Better returns than Buffett produced in the first five years of his career.

- I’d continue working this process to compound our value for the long-term.

Over a one to five-year period the plan is to continue to grow the acquisition and build as much value as possible, pay off debt, invest the stock market funds at Rivera Holdings, continue to produce a ton of excess cash flow at the subsidiary acquisition, and compound value of all investments and assets owned.

I wouldn’t look to do another full acquisition within the first two years after the first acquisition closes unless something ultra cheap and attractive falls into our laps.

The plan within the next five to ten years is to either take Rivera Holdings public through an IPO or to buy enough of a public company to do a reverse merger onto the stock market.

There are two ways you can make money owning shares in Rivera Holdings over the long-term:

- The first is holding Rivera Holdings private shares while they compound value over the next five to ten years until the company goes public and your shares become worth a lot more.

- The second is holding your Rivera Holdings private shares for a few years and then reselling them to Rivera Holdings after they’ve appreciated in value and/or you’ve earned your initial investment back plus a return you’re comfortable with.

Conclusion

This is a fantastic opportunity for us all to buy a massively undervalued business for half of its true worth.

This is a fantastic opportunity to buy into a 60%+ net profit margin business that already produces a ton of excess cash we can use to buy other valuable assets that also has huge room for growth in sales and profitability.

This is a fantastic opportunity to buy into a business that has a gigantic government/regulatory moat built around it.

This is a fantastic opportunity to buy into a business with a huge margin of safety and huge protections around it that give us an even bigger margin of safety.

This is a fantastic opportunity to buy into a business that will grow in value between 39.3% and 54.8% each year for the next three years. Or produce a cumulative – non-compounded – return after three years of between 117.9% and 164.4% over three years.

This is a fantastic opportunity to get in at the early stages towards building a billion dollar plus company.

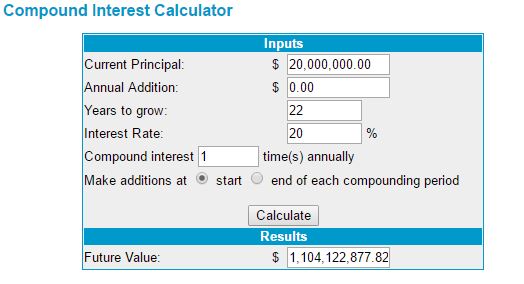

Below is a chart illustrating this. At a 20% rate of return – far below the 31.1% I’ve produced each year for the last five years not compounded – and with no new capital contributions, it will take us only 22 years to compound a capital base of $20 million into more than $1 billion.

And I want you to become part of this fantastic opportunity for long-term wealth creation and appreciation as we build something great.

If you’re interested in learning more about the great business we’re acquiring please sign and return to the below email address the short two page NDA to receive more information about the target acquisition.

Or if you already want to invest in Rivera Holdings please contact me at either 605-390-3157 or JasonRivera@valueinvestingjourney.com

Sincerely yours,

Jason M. Rivera

Chairman, CEO, and Founder of Rivera Holdings

NDA below here.

By signing the below agreement The Seller of acquisition target has agreed to let me tell potential Rivera Holdings investors more information about the target acquisition. This includes what the business is, what industry it operates in, more specifics about its operations, and our – Rivera Holdings – plans after acquisition of target business closes.

For convenience the NDA can also be downloaded and printed off by clicking the following link.

***

THIS AGREEMENT is made and entered into as Nov 7, 2016 (“Effective Date”), remains effective until the close of acquisition and/or Rivera Holdings and The Sellers agree to not do sale, by and between Rivera Holdings, (“the Disclosing Party”) and _____________________________ Your Name In Space, (“the Recipient”) (collectively, “the Parties”).

Purpose for Disclosure (“Business Purpose”): The purpose of this agreement is to protect both The Seller, Rivera Holdings, and yourself (potential investor) from breaching any legal, competitive, or fiduciary agreements made between the parties prior to acquisition of target company.

The Parties hereby agree as follows:

- For purposes of this Agreement, “Confidential Information” shall mean any and all non-public information, including, without limitation, technical, developmental, marketing, sales, operating, performance, cost, know-how, business plans, business methods, and process information, disclosed to the Recipient. For convenience, the Disclosing Party may, but is not required to, mark written Confidential Information with the legend “Confidential” or an equivalent designation.

- All Confidential Information disclosed to the Recipient will be used solely for the Business Purpose and for no other purpose whatsoever. The Recipient agrees to keep the Disclosing Party’s Confidential Information confidential and to protect the confidentiality of such Confidential Information with the same degree of care with which it protects the confidentiality of its own confidential information, but in no event with less than a reasonable degree of care. Recipient may disclose Confidential Information only to its employees, agents, consultants and contractors on a need-to-know basis, and only if such employees, agents, consultants and contractors have executed appropriate written agreements with Recipient sufficient to enable Recipient to enforce all the provisions of this Agreement. Recipient shall not make any copies of Disclosing Party’s Confidential Information except as needed for the Business Purpose. At the request of Disclosing Party, Recipient shall return to Disclosing Party all Confidential Information of Disclosing Party (including any copies thereof) or certify the destruction thereof.

- All right title and interest in and to the Confidential Information shall remain with Disclosing Party or its licensors. Nothing in this Agreement is intended to grant any rights to Recipient under any patents, copyrights, trademarks, or trade secrets of Disclosing Party. ALL CONFIDENTIAL INFORMATION IS PROVIDED “AS IS”. THE DISCLOSING PARTY MAKES NO WARRANTIES, EXPRESS, IMPLIED OR OTHERWISE, REGARDING NON-INFRINGEMENT OF THIRD PARTY RIGHTS OR ITS ACCURACY, COMPLETENESS OR PERFORMANCE.

- The obligations and limitations set forth herein regarding Confidential Information shall not apply to information which is: (a) at any time in the public domain, other than by a breach on the part of the Recipient; or (b) at any time rightfully received from a third party which had the right to and transmits it to the Recipient without any obligation of confidentiality.

- In the event that the Recipient shall breach this Agreement, or in the event that a breach appears to be imminent, the Disclosing Party shall be entitled to all legal and equitable remedies afforded it by law, and in addition may recover all reasonable costs and attorneys’ fees incurred in seeking such remedies. If the Confidential Information is sought by any third party, including by way of subpoena or other court process, the Recipient shall inform the Disclosing Party of the request in sufficient time to permit the Disclosing Party to object to and, if necessary, seek court intervention to prevent the disclosure.

- The validity, construction and enforceability of this Agreement shall be governed in all respects by the law of the Delaware. This Agreement may not be amended except in writing signed by a duly authorized representative of the respective Parties. This Agreement shall control in the event of a conflict with any other agreement between the Parties with respect to the subject matter hereof.

IN WITNESS WHEREOF, the Parties have executed this Agreement as of the date first above written.

___________________________________________________

Your Signature

___________________________________________________

Your Printed Name

***

Remember to sign and return the above NDA to JasonRivera@valueinvestingjourney.com to receive more information about the target acquisition.